Services

Sectors

Our Work

Why Apadmi?

Careers

Insights & Events

Contact

Services

Sectors

Our Work

Why Apadmi?

Careers

Insights & Events

Contact

Services

View all services

Defining your product vision with insight and innovation

Technology strategy

Product strategy

Digital transformation

Innovation

App audit

User research

Designing and engineering transformational products

Mobile app development

Complex system integrations

Website development

UX and UI design

Team augmentation

Accessibility

Performance through support, optimisation and analytics

Data science and analytics

Monitor, support and maintain

Product optimisation and conversion

Our Work

View all work

BBC iPlayer Radio

Chelsea FC

McCain

Domino's

The Wonder Weeks

NHS - DonorPath

Lexus

Co-op Health

Big Issue North

My First Five Years

United Utilities

SailGP

Argos

Vodafone

BBC iPlayer Radio

Insights

Events

News

Resources

View all

News

28/11/2024

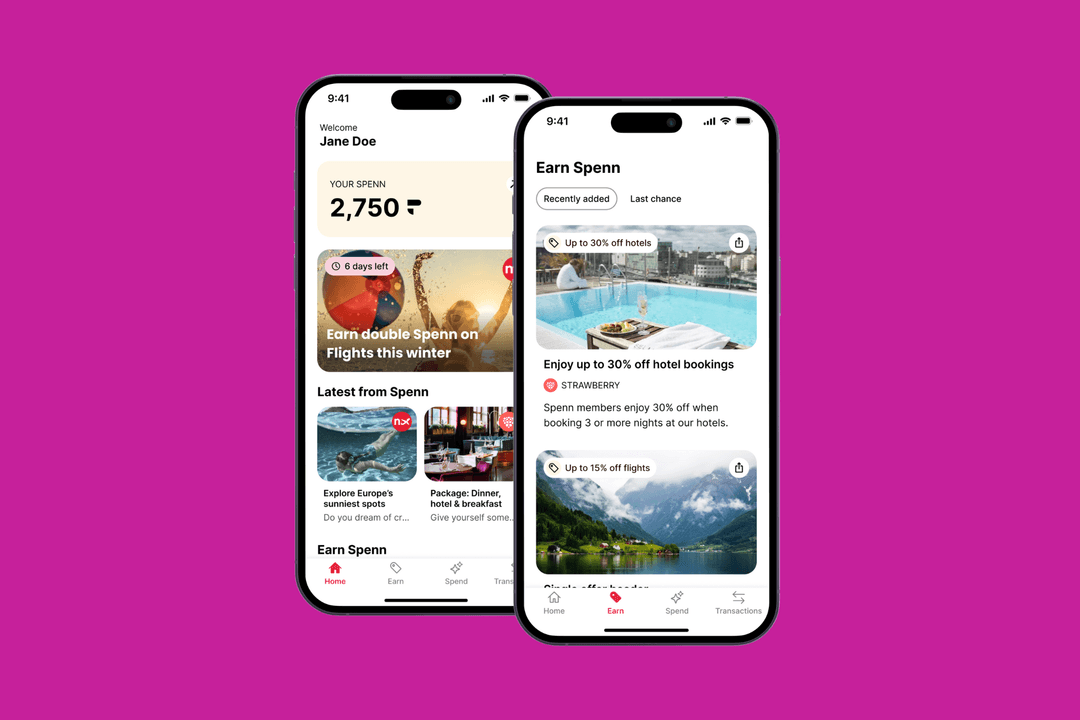

Apadmi partners on new chart-topping loyalty currency app Spenn

27/06/2025

Insights

How mobile-first strategies are reshaping digital experiences

28/04/2025

Resources

App Champions Index 2025

10/07/2025

Events

Roundtable: The future is personal - unlocking AI-Driven customer experiences with Bloomreach

Sectors

View all sectors

Retail

Finance

Healthcare

Sport

Telecomms

Utilities

Retail

Home

insights

Thoughts, news and events

The latest from our world and things we've found interesting from everybody else's.

Jump To

Insights

Events

News

Apadmi Asks

Resources

Insights

View all

Events

View all

News

View all

Resources

View all

Loading...

Apadmi Asks

View all