Why the buy side of agentic commerce is the problem nobody’s solving

There’s a conversation happening across every large commercial organisation right now about agents. It goes something like this: agents are coming, we need an agent strategy, how do we make sure agents find us? That instinct is right, but the sequencing is wrong — and the sequencing matters, because getting it backwards means building the wrong thing at the wrong time for the wrong reason.

Let’s explore the landscape as it actually stands today, rather than how it appears in strategy decks.

What’s deployed today is chatbot commerce, and it comes in two flavours

In the platform-mediated version, a user talks to ChatGPT, Gemini, or Claude and asks it to find a flight. The LLM recommends something, a protocol stack connects that recommendation to the supplier’s booking system, the transaction completes without the user leaving the chat window, and the LLM provider takes a referral fee. This is Google search ads rebuilt for a conversational interface — the user thinks they have an agent, but what they actually have is a shop assistant who works on commission.

In the retailer-embedded version, the chatbot lives inside the retailer’s own app or website. The user talks to the airline’s chatbot, it populates the basket, the user checks out within the airline’s own surface. No intermediary, no referral fee, and the brand relationship is preserved. This is a UX improvement rather than a channel shift — a legitimate defensive move against the platform-mediated model.

Look under the hood of either version and the “agentic” part evaporates. When ChatGPT “buys” something from a retailer, it’s calling a structured API — product discovery, cart management, checkout endpoints. OpenAI’s Agentic Commerce Protocol has four REST endpoints. That’s a well-designed shopping cart interface, not agent-to-agent negotiation — the retailer is running a shop with an API. A significant amount of protocol work (ACP, UCP, and the associated product feed standards) is going into making seller platforms directly visible and queryable by the chat platforms, which makes this model work better but doesn’t make it agentic.

These are necessary first steps. The emerging protocol infrastructure (Google’s A2A, Anthropic’s MCP, Visa’s TAP, Mastercard’s Agent Pay) is genuinely designed for the full spectrum, from chatbot checkout to autonomous agent-to-agent negotiation. But the current commercial deployments are all at the chatbot end, because that’s where the users are today.

What’s coming next is the proliferation of personal buyer agents

This is the step that changes everything. Not sell-side agents or new protocols — buyer agents. Autonomous software acting on the user’s behalf, with its own tools, its own information sources, no channel loyalty, and no inherent reason to complete a transaction in any particular place.

The demand signal is already clear. OpenClaw — a solo developer’s side project, vibe-coded and genuinely painful to configure — went from launch to 180,000 GitHub stars to OpenAI acqui-hire in sixty days, because it actually controlled applications, booked flights, managed inboxes, and completed tasks across platforms. If people are willing to wrestle with day-zero open-source cruft to get a working personal agent, companies will ship polished versions given time. OpenAI hired the developer behind OpenClaw - the direction is unmistakable.

When these agents do arrive, they won’t limit themselves to the platform-mediated chatbot commerce pipe. They’ll use your API if that’s the best route, your website if there’s a promo code the API doesn’t honour, a consolidator if the net fare is lower. They’ll have unlimited patience, real-time access to competitor pricing, and no commitment to completing a transaction where they started the conversation. They’ll compare and shop across all your channels, and pick the one that suits their user best – regardless of your channel strategy.

That buyer-side pressure is what will actually justify building non-trivial sell-side agents

Not the generic “we need an agent strategy” from a conference deck, but a specific commercial need. When buyer agents start collapsing your channel strategy and compressing your margins by playing a one-dimensional price game across every surface you have, the only rational response is to move the conversation off price and onto dimensions where you can create value. You can’t do that through a checkout API. You need a system that can negotiate, differentiate, and make the case for your product in ways a product feed never could. The sell-side agent is a defensive response to buyer agent proliferation, not step two in a technology roadmap — and understanding what you’re defending against is the prerequisite for building it well.

That’s what this article is about. Not the sell side, not the protocols — the buy side. What’s coming through the door, what it looks like, what drives it, and why the answers to those questions should shape every agent investment the sell side makes.

Four agents walk into an airline

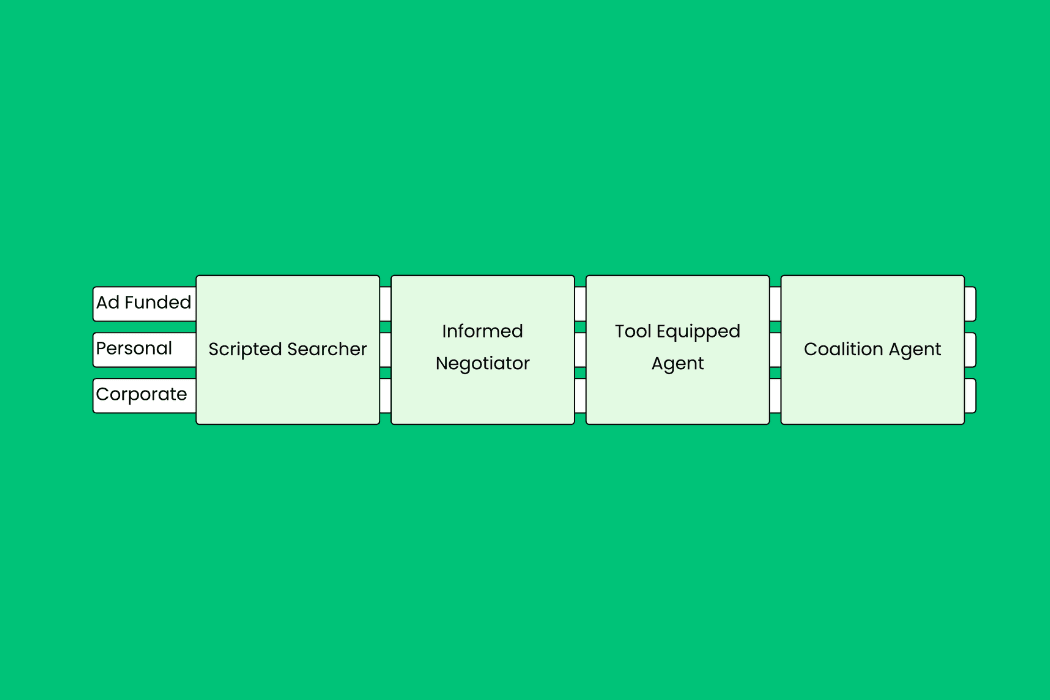

Let me make this concrete. Imagine you’re an airline — though the dynamics apply to hotels, retailers, insurers, or anyone selling something with variable pricing and finite inventory. Four different buyer agents arrive at your system within the same hour, all looking for the same route on the same date. They’re all “agents,” but they have almost nothing else in common.

The Scripted Searcher is what most people picture when they hear “AI travel agent.” A chatbot with preferences strapped on — it searches, filters, and presents results, with no real negotiation capability and no contextual awareness beyond what the user typed in. This is where most commercial “AI agents” sit today, barely distinguishable from a competent autocomplete.

The Informed Negotiator has the user’s full context — calendar, budget, loyalty status, trip purpose, date flexibility. It can engage in multi-turn negotiation and make genuine trade-offs: “I’ll take the 06:40 connection if you can offer the upgrade.” The information is loaded at session start, but the negotiation is real. This is the archetype most prototypes are designed against.

The Tool-Equipped Agent has everything the Informed Negotiator has, plus live access to external information mid-conversation — competitor fares, real-time loyalty balances, the airline’s own promotional pricing that the API doesn’t surface. Its advantage isn’t access (a determined human could do the same); it’s unlimited patience applied to a process most humans abandon after ten minutes.

The Coalition Agent isn’t acting alone. This archetype opens up three dynamics worth separating: demand aggregation (agents consolidating group demand at machine speed without the humans planning to coordinate), inter-agent intelligence sharing (real-time competitive data from parallel negotiations), and information brokering (pooled completion prices creating a market transparency layer that doesn’t currently exist in consumer travel).

When channels stop being separate

The Tool-Equipped Agent deserves particular attention, because it’s the archetype that breaks channel strategy. Airlines, hotels, and retailers have spent decades building channel-specific pricing — different fares through the website, the GDS, NDC, consolidators. Revenue management depends on this segmentation. A Tool-Equipped Agent treats all channels as a single queryable surface and finds the best option across the lot.

Critically, this agent has no commitment to completing the transaction where it started the conversation. It might negotiate with your sell-side agent, extract your best offer, and book through a consolidator because the net fare is lower. There’s an assumption in much of the agentic commerce discourse that the agent-to-agent channel will naturally offer the best deals — because it’s direct, because it cuts out intermediaries. That’s not how distribution works. Consolidators have negotiated net fares below anything the direct channel can offer. A buyer agent that restricts itself to the agent-to-agent channel is, by definition, a worse agent than one that shops everywhere.

There’s a subtler problem too. The sell side won’t know where it sits in the buyer agent’s journey. Is this the first exploratory query from an agent early in its search? A follow-up from an enquiry made an hour ago, or a day ago? The start of actual execution? The entire path to purchase becomes obscured, and a seller may never know when they’ve been qualified out of a sale — never get the chance to provide the one piece of information that would have kept them in contention.

Same engine, different driver

The archetypes describe what buyer agents can do, but capability isn’t the dimension that matters most. Two agents with identical toolkits will behave in fundamentally different ways depending on who’s paying for them.

The ad-funded agent is the one most consumers will encounter first, because it’s free. It’s also, structurally, chatbot commerce wearing the clothes of agentic commerce — the ordering, emphasis, and recommendations shaped by whoever’s paying for placement. An ad-funded Tool-Equipped Agent looks like it’s working for you, but it’s optimising for commission yield: steering toward carriers with higher affiliate payouts, “failing” to surface cheaper options that would cost its operator revenue.

If this sounds theoretical, it shouldn’t. The UK’s motor finance commission scandal and PPI followed exactly this structural pattern — an intermediary nominally acting for the buyer, actually optimised for the seller’s commission. The regulatory framework for dealing with commission-conflicted intermediaries already exists. It just hasn’t been applied to software yet.

The premium user-aligned agent is what you get when the user is the customer — a subscription service, or a built-in capability from whoever wins the personal-agent market. No commercial relationship with the seller, no reason to reveal its user’s preferences, no channel loyalty. It will open a negotiation with your agent and close through a consolidator without a second thought. It anchors low, waits patiently, and exploits every information asymmetry available. For airlines, hotels, and anyone with perishable inventory, this is the agent that compresses margins.

The managed corporate agent sits between the other two — operated by an employer or TMC, with policy constraints, preferred carriers, and approval workflows. Less price-sensitive, more predictable. The counterpart the sell side secretly wishes they all were.

The critical insight: a Tool-Equipped Agent funded by advertising is fundamentally different from one paid for by the user, even with identical capabilities. The first might trade user value for commission and stay in its own channel. The second will use every tool and every channel to optimise for the user’s preference. Same engine, completely different driver.

When both sides learn

Everything described so far treats the archetypes as static, but these agents will learn — or more precisely, the infrastructure around them will. A user-aligned agent that negotiates thousands of bookings develops a statistical model of pricing behaviour: which carriers drop fares before departure, which respond to competitive pressure, which concede on bundles more readily than on base fare.

More likely than individual agents learning in isolation is the emergence of negotiation intelligence services — paid tools that pool anonymised transaction data across thousands of agents. An agent doesn’t need to have personally negotiated ten thousand bookings if it can subscribe to a service that has. Of course, data protection constraints are real: GDPR doesn’t care that the primary purpose is commercial intelligence – but they’re design constraints to be worked with, not a reason not to build something.

The sell side will learn too. Over time, sell-side systems may recognise that certain patterns of agent interaction are disproportionately margin-negative — the sophisticated agents that only show up when a fare is mispriced or competitive pressure creates an unusually good deal. The rational response goes beyond negotiating differently — it extends to questioning whether to negotiate at all. Tighter identity requirements, less generous offers to unidentified agents, or declining to engage with traffic that pattern-matches to informed counterparts.

One plausible outcome: instead of channels collapsing into one transparent market, they deliberately re-fragment. Premium loyalty channels, corporate procurement rails, platform-controlled agent surfaces, public price endpoints — each with different access levels, pricing, and rules of engagement. The endgame might not be transparency — it might be a more sophisticated kind of opacity. When both sides are autonomous, learning, and optimising at machine speed, the dynamics start to resemble the algorithmic environments that financial markets have grappled with for decades.

Designing for the counterpart you can’t predict

The sell side doesn’t get to choose its counterpart. What walks through the door will range from a scripted chatbot to a tool-equipped agent with real-time market intelligence, from a commission-optimised intermediary to a premium personal agent that will methodically extract every pound of value your system will give. You won’t be able to tell, from the outside, which one you’re facing.

That means testing against all the archetypes, including the adversarial ones. It means understanding that the buyer-side pressure is what justifies your sell-side investment — and that an investment shaped by the counterparts you’ll actually face looks very different from one shaped by conference-deck optimism.

There is an alternative: don’t participate. Stay with the checkout API, accept that the platform owns the customer relationship, and compete on operational efficiency alone. For some businesses that’s a legitimate strategic choice — but it’s a one-way door, and the price is every lever except fulfilment.

The entire current commercial deployment is chatbot commerce — platforms calling checkout APIs. The protocols support genuine agent-to-agent interaction, but nobody’s deployed it for commerce yet. The buyer agents that will force that evolution are coming. The organisations that thrive will be the ones that understood the buy side before they built the sell side — and designed for the counterparts they didn’t choose.

In my next piece, “Why a checkout API won’t be enough,” we'll explore the practical implications: what a sell-side agent actually needs to do, how to handle negotiation in natural language without hallucinating offers you can’t honour and why information and differentiation matter as much as price. We'll also look at how loyalty programmes need to evolve when the customer’s representative thinks in expected value.

Share